Concerned & Looking for Information

Most people have more options than they know. And when they learn that they have more options, they get confused about which one to choose.

But it’s not that difficult. Here’s how to do it.

1. Identify all options that could apply to your situation. Not all will, but you will normally have several that you could choose from.

2. Evaluate the ones that you could use. Compare against each other.

3. Choose the top one or two that make sense, and seek a free consultation for more info.

This simple, 1 – 2 – 3 approach breaks down the complicated problem into easy-to-do steps.

Let’s begin.

Most people have more financial solution options than they are aware of. In fact, there are at least SIX options you need to know about.

Six Options

There are six main considerations for debt relief, and advanced strategies that combine several of them for a highly customized solution. Knowing these financial solutions will help you understand what you can do.

Three Non-Bankruptcy Options:

1. Credit Counseling

Credit counseling is probably the most common (and least powerful) debt relief program. It can be effective if your debts are not seriously out of control, and you just need some help creating a budget or controlling your spending.

A credit counselor reviews your income and expenses with you and looks for ways to cut out your non-essential expenses. It’s not really debt reduction, but it is expense reduction. But, for some folks, this is all that is needed.

2. Debt Management Plans

This is the program you see plastered all over television and the internet. DMPs promise to get you out of debt in a short time without filing bankruptcy. These programs can be effective, depending on the amount and kinds of debt you have. They are not for everyone, and can get you sued.

DMPs will attempt to negotiate a lower interest rate, better payment terms, or even possibly (but rarely) get the creditor to forgive some of the debt. You end up paying taxes on any debt forgiven, so the “amount saved” is less than it appears.

DMPs are entirely voluntary – creditors sometimes refuse to participate. These plans will lower your credit score, because you are “not paying as agreed” but if you have the right kind of debts, and if you don’t owe too much, a DMP may work for you.

IMPORTANT! Many DMPs are just scams. They take your money and do little or nothing. Then you get sued. Be extremely cautious when hiring one of these companies.

3. Debt Settlement

The debt settlement model is more extreme (and dangerous) than a DMP. In a debt settlement program, you hire a company and start paying them, not your creditors. Your credit score drops like a rock, as you get further and further behind in your payments

Your debts will go to collections, and that’s when the debt settlement process begins. The money you have paid to the company is used to attempt to negotiate lump sum settlements with your creditors. You pay tax on any debt that is forgiven.

Some creditors won’t settle. They sue instead. The debt settlement company can’t help you when you are sued, and will refer you to a bankruptcy attorney. I see a lot of bankruptcy cases result from failed attempts at debt settlement.

Two Bankruptcy Options

Bankruptcy is a powerful and effective debt relief tool. More people should file bankruptcy than do because they don’t understand how it works, and how quickly they can rebuild their credit after discharging their debts in bankruptcy.

4. Chapter 7

More people file Chapter 7 than any other kind of bankruptcy. Although it is referred to as a “liquidation bankruptcy” most of my clients keep everything they want to keep, and get rid of what they want to get rid of, including all their credit card bills, medical bills, and other unsecured debt. They pay for what they want to keep, like their house and vehicles.

Some debts cannot be discharged in Chapter 7, like child support, student loans, and most taxes (although older taxes are frequently dischargeable!).

Chapter 7 cases are short, about 5 months from beginning to end. You have to list all your creditors, list all your debts, and provide a detailed financial history. You do not appear before a judge. There is a brief trustee meeting where you confirm that the information you put in your bankruptcy petition is complete and correct.

Rebuilding credit after Chapter 7 is not hard if you know how. As a certified credit counselor, I have created a very effective program to help my clients recover their credit quickly after discharging their debt in Chapter 7. Typically, my clients get credit scores of 650 – 700 within one year of their discharge.

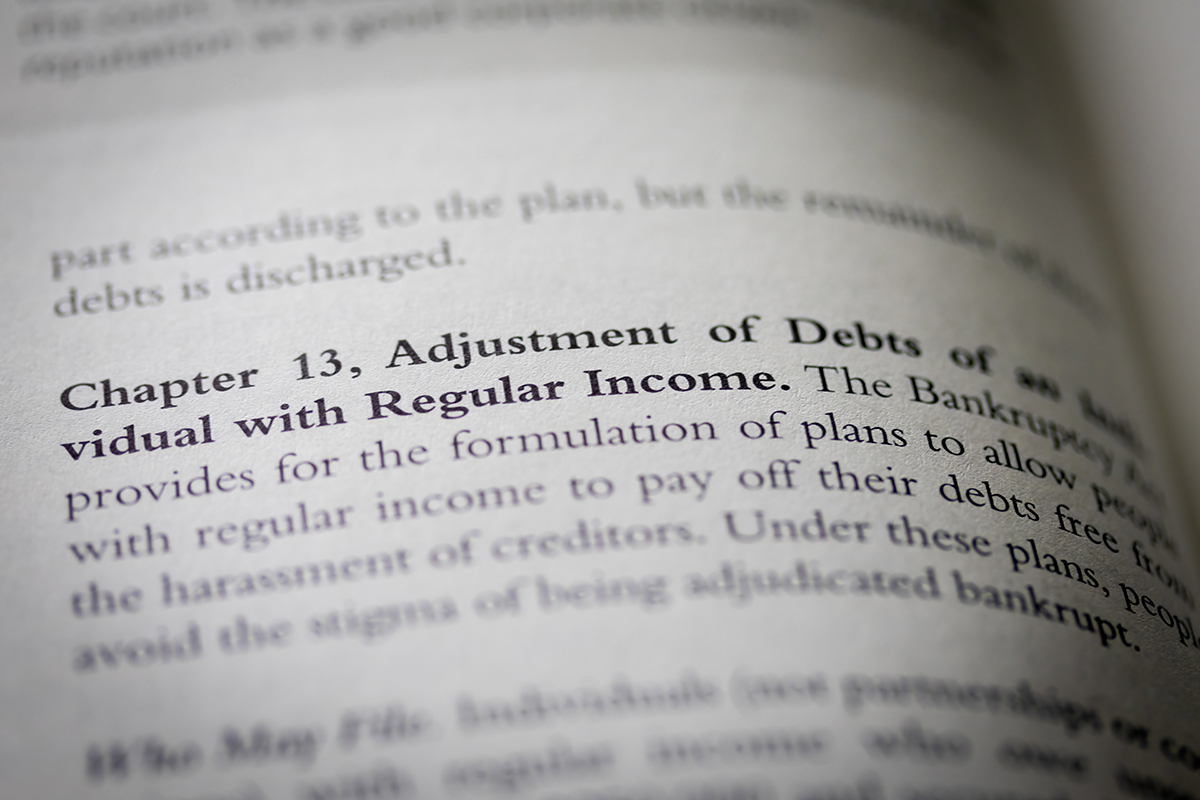

5. Chapter 13

Chapter 13 is the most powerful, and most misunderstood debt relief program we have. Many attorneys do not fully understand what can be achieved with Chapter 13.

As a result, Chapter 13 is underutilized, and I see many people who file Chapter 7

“leave money on the table” because they should have been advised about their options in Chapter 13.

Chapter 13 is a payment program, but seldom does anyone pay all their debt. In most of my Chapter 13 cases, we only pay a single penny on the dollar to unsecured creditors. We catch up on missed payments for property we want to keep, like cars and houses, and wipe out everything else.

Most people who qualify for Chapter 7 also qualify for Chapter 13, and should insist that both options be fully explored and evaluated by any professional they visit, so they can make a fully informed decision when comparing the two types of bankruptcy options.

The Last Option

6. A Final Option

A final option – deliberately decide to refrain from any of the above options.

Either permanently or for the time being. You deliberately decide to “not do” something. This is a choice. This is an often overlooked option.

Consider this example. Imagine that you’re on Social Security. You have a fixed income, barely enough to get by. Certainly not enough to pay any of your bills.

Most creditors cannot garnish your Social Security check. And, if you don’t have any property they can attach, you are “uncollectible.” Even if they sue you and get a judgment against you.

Now, this option is not without its price. Creditors can be ruthless and wear you down.

- They are permitted, by law, to attempt to collect their debt.

- They can sue you.

- They can call you. And call you. And call you.

- They can send you nasty letters.

- They can make your life miserable.

But they can’t take what you don’t have (you want to discuss this with an attorney, though, so you will be sure what is protected and what is not).

And they can’t take income that is protected by law.

More Advanced Strategies

Because I’ve been helping people solve debt problems for over 35 years, I’ve learned that sometimes it is best to combine one or more strategies to get the best results.

For example, you might lose your job and become uncollectible for a period of time.

When you become reemployed and we might pursue a debt settlement program or a debt management program. If that works – then the problem is solved.

Depending on circumstances, the amount of debt that you owe, etc., you might try a non-bankruptcy option for a period of time and later realize that it is not getting you out of debt fast enough. At that point in time you’d want to consider pursuing one of the bankruptcy options that might be available to you.

There are even “strategies within strategies” I use to preserve even MORE options for my clients.

For example, let’s imagine you have an aging parent who you are caring for in your home. Perhaps the parent will be passing away soon, or, perhaps you still have children living with you, struggling to get out on their own and they are just not able to move out yet.

In these situations, you may need to keep the home you have for a few more years. We might consider keeping the home in a chapter 13 for 3 or 4 years, and then converting the chapter 13 to a chapter 7, and discharging the entire debt, and you emerge free of that huge mortgage on the upside-down house.

This is an advanced strategy which solves multiple problems.

As you can see, to get the best results, you have to have the best coach. You need someone who is trained and certified and has years of experience in all of the different debt relief strategies in order to be sure that you have the right formula for getting out of debt.

And, there’s even more…

Once you are achieving your goal of getting out of debt, there are two additional and very important aspects of your financial health that you need to address.

One, you need to rebuild your credit.

You may think it’s premature to think about rebuilding credit while you’re in the middle of the debt crisis. However, if you get the right expert on your side you will soon be on your way out of debt. While you are getting out of debt, you need to be rebuilding your credit. Yes, you can do both at the same time, if you know how.

Finally, your credit report needs to be professionally reviewed.

I teach my clients what to do to rebuild their credit and also how to quickly and effectively review their credit report for errors that affect their score. Some errors do, and some don’t, so it’s important to know the difference.

When you think of your financial problems, do you feel worried? Even a little sick to your stomach? You’re not sure what to do, but you’re sure you need to do something. You’re at the stage where you know you need help, but don’t know what kind of help or where to get it.

To get the solution you need, just take our “crash course” in debt relief options. To solve serious debt problems, you can zero in on just two kinds of solutions. It won’t take you long to review them and get feel for if you need bankruptcy or if a non-bankruptcy program will work for you.

Two Main Options for Serious Debt Problems

- Non-Bankruptcy Programs.

- Debt Management Program.

You cannot watch television or surf the net without seeing advertisements for debt management plans.

These plans promise to wipe out your debt in a short time without filing bankruptcy. Not for everyone, though, because their effectiveness depends on many things. Individual results vary widely, depending on the amount and kinds of debt you have. They do not work for everyone. When they fail, you are often sued by your creditors.

With a DMP, you try to negotiate lower interest rates, better payment terms, or even possibly some debt forgiveness. Remember that you always pay taxes on any debt forgiven.

And, because DMPs are totally voluntary, some of your creditors won’t go along with them. And, these plans lower your credit score, because you are behind while in these plans. However, if you have the right kind of debts, and if you don’t owe too much, this may be worth checking into.

Warning! I’ve seen many DMPs turn out to be scams that take your money and leave you hanging out to dry. They perform no service, and then disappear. Then you get sued. You need to check them out and read your contract before getting involved with one of these.

Debt Arbitration or Debt Settlement

With the debt settlement model, you hire a company and start paying them instead of your creditors. Your credit score will drop, sometimes more than 100 points, as you get further and further behind in your payments.

Making no payment on your debt results in your accounts being sent to collections. This is the desired result in debt settlement, because it is easier to make a settlement with a collector than it is the original creditor. My clients tell me they find the entire process unnerving.

Obviously, not all of your creditors will play this game. Some won’t settle. They sue you. Then you have not only the debt, but the law suit on your credit report. When one creditor sues, others often follow.

A debt settlement company is not a law firm. They cannot represent you in court when you’re sued. All they can do is refer you to an attorney. Then, in many cases I see, we discover that the client should never have been in the program in the first place, because bankruptcy was the best choice all along.

Bankruptcy Solutions

Chapter 7

Chapter 7 is the most popular bankruptcy chapter for good reason. This is the fastest way to wipe out debt, keep your property and quickly rebuild your credit.

When done right, and followed by the proper credit recovery program (which is NOT part of bankruptcy – so no attorneys I know of provide this program but West Law Office) it can be the most effective debt relief program for you.

Don’t be misled by what you read on the internet about chapter 7. Even though it is referred to as a “liquidation bankruptcy” you will usually keep all your property. If it is “secured” like your house or car, you will continue to pay those debts.

Most debts are discharged in chapter 7, but some debts cannot be discharged. Examples of non-discharged debts include child support, student loans and most taxes (although some older taxes are dischargeable!).

Chapter 7 cases only last 5 months. There is no court hearing, just a meeting with a trustee. You’ll fill out a very long questionnaire for your attorney and provide a comprehensive list of documents. Your attorney is responsible for making sure you don’t have any issues or problems which would cause you to lose property or have your case dismissed.

This is important, so you should consult a board certified specialist to ensure your case is properly handled.

Chapter 13

Chapter 13 is the most powerful, yet the most misunderstood bankruptcy chapter.

Chapter 13 offers more options than chapter 7 and you could actually pay less for property you keep if you file chapter 13 instead of chapter 7. Sadly, many attorneys will only consider chapter 7 if their client qualifies for chapter 7. That’s why it’s important for you to compare both options before you make a final choice about which chapter to file.

You do not pay back all your debt in chapter 13 in most cases. Although chapter 13 is a payment plan, these plans may only pay a single cent on the dollar to your unsecured creditors. It’s actually very close to a chapter 7 in this regard.

Chapter 13 is a good choice for catching up on missed payments for property you want to keep, like cars and houses, and lets you wipe out everything else for virtually no payment at all.

Remember, if you qualify for chapter 7, you probably also qualify for chapter 13. It’s very important that you be sure to compare both options. To make sure you have the best option for your situation, only consult with a firm that specializes in bankruptcy and files both chapters regularly.

Summary

If you can afford to pay off 80% of your debt in the next 3 years, then you may want to try a debt management or debt settlement program. If you don’t truly think your situation is that serious, these programs can be effective, although in my experience it will hurt your credit for much longer than if you file bankruptcy and immediately begin to rebuild your credit after discharging your debt.

If your debt problems are more serious, or if you just want a faster financial recovery, bankruptcy offers a more powerful option. My clients find that their finances, and credit score, recover much more rapidly with the bankruptcy option.

This is because, in my office, we combine debt discharge with a proven program to rebuild your credit and clean up your credit report as part of your overall financial recovery plan.

Serious money problems will paralyze you – make you feel overwhelmed and confused so you don’t know what to do. If you have problems this bad, you probably need to look into filing bankruptcy.

And you need the best advice and counsel to make sure you get the right solution.

Don’t rush into anything. Do some reading, and learn the basics. That way you’ll have a better understanding. Then get an expert to help you wipe out your debt, keep your property, and rebuild your credit. Read the reviews, find out what actual clients say about their own cases.

Serious problems demand serious solutions. Bankruptcy is often referred to as the “last resort” to be tried only after you have tried, and failed, all other options. But . . .

This is really, really bad advice.

Think about this a second. If your doctor tells you that you need surgery, are you going to waste your time trying other “less serious” treatment programs? Or, are you going to fix the problem and get on the road to recovery. I know what I would to do. And I wouldn’t waste any time, either. Neither should you.

Bankruptcy Basics – how to know which is best

For serious debt problems, you need to become familiar with chapter 7 and chapter 13, and how they compare against each other. Although more people file chapter 7 than 13, many of these folks “leave money on the table” because they fail to adequately compare the two options.

To make things worse, many attorneys I know will always recommend chapter 7 if you qualify for it – without even comparing the benefits of chapter 13. Their clients don’t know they could have received a better result in chapter 13.

Don’t make this mistake. It could cost you thousands of dollars.

If you qualify for chapter 7, you probably also qualify for chapter 13. You should “do the math” and figure out how much better off you will be if you file chapter 7 and compare it to how much better off you’ll be if you file chapter 13.

This is not hard. It’s like doing your taxes if you’re married. You do them individually, and then jointly, and see which way you get the best result. Same here.

Chapter 7 Bankruptcy

Key points:

- Most popular. More people file chapter 7 than chapter 13

- Won’t lose property. Although referred to as a “liquidation bankruptcy” truth is you generally keep all your property and lose nothing.

- Faster credit recovery. If you have the proper program, like ours here at West Law Office, it’s possible to recovery your credit after filing chapter 7 very quickly. Our clients generally report credit scores of 650 – 700 within one year of discharge.

- Takes only about 5 months from beginning to end. Unlike a chapter 13 which is 3 to 5 years.

Chapter 7 will totally eliminate most unsecured debts, like credit cards and medical bills. Personal loans, payday loans, and lawsuits are also wiped out. Debts which are secured, like houses and cars, can be kept in chapter 7, and you continue to pay these debts as if you had not filed bankruptcy.

Chapter 13 Bankruptcy

Key Points:

- More powerful and flexible than chapter 7. Experienced attorneys can get better results, meaning you pay less, than in a chapter 7 for some clients.

- Can stop repossession and foreclosure. Unlike chapter 7, where you need to be current on property you want to pay for and keep, the chapter 13 is designed to force your creditors to let you catch up missed payments.

- Pay less for secured debts, like cars and jewelry. Unlike chapter 7 reaffirmations, where the terms of your contract stay the same, chapter 13 will lower your interest rate to about 5%. This can save you hundreds of dollars or more.

- Pay less than what you owe for property you want to keep. If you purchased your car more than 910 days ago, or other secured property more than a year before you file, you only have to pay the value of the property, not what you owe on it. This can save you thousands of dollars.

Chapter 13 is a payment plan, but this doesn’t mean you have to pay all your debts. Sometimes you pay only 1% of your unsecured debt, and your “payment plan” only pays for things you want to keep, like your car and house.

Chapter 13 plans are from 3 to 5 years long. Many people think this is a negative but if you consider that most of us have car payments that are in that range, it’s easy to see that the chapter 13 is really not any different than just having a car payment. And, since you pay off your car in the case, most of the time your household budget has more money in it than if you had filed a chapter 7.

Comparing Chapter 7 vs Chapter 13

One is not better than the other. They are different. Depending on your unique circumstances and your personal goals, one will normally be better for you than the other.

That’s where it really helps to have an experienced specialist listen to your story and goals. Over the last 35 years, I’ve helped over 20,000 people find the right solution to their difficult debt problems. I’ve probably solved the exact problems you have hundreds of times.

What to do next…

Now that you understand the differences between chapter 7 and 3, and how they compare, you’re ready to get some expert help to create the recovery plan that’s best for you. It’s not going to be “all new” to you since now you already know the basics.

To be successful, remember this… don’t just settle for getting a bankruptcy discharge. That’s only the beginning. The bankruptcy discharge is often called a fresh start. But it’s only a start. Only the beginning of what you need for a full financial recovery.

You need to finish what you start. That’s the critical piece that’s missing in other law firms. They don’t have a program like ours to help you get the credit recovery that finishes the job that bankruptcy only starts.

At West Law Office, we’ve been helping our clients finish the job that bankruptcy only starts for many years. Our proven program of credit recovery and credit report correction is the key to getting the result that bankruptcy promises, but, by itself, cannot deliver.

You’re now ready to take the next step. Contact us for a free consultation and let us design your plan for a full financial recovery. The consultation is free, but the results can be life-changing.